Share this @internewscast.com

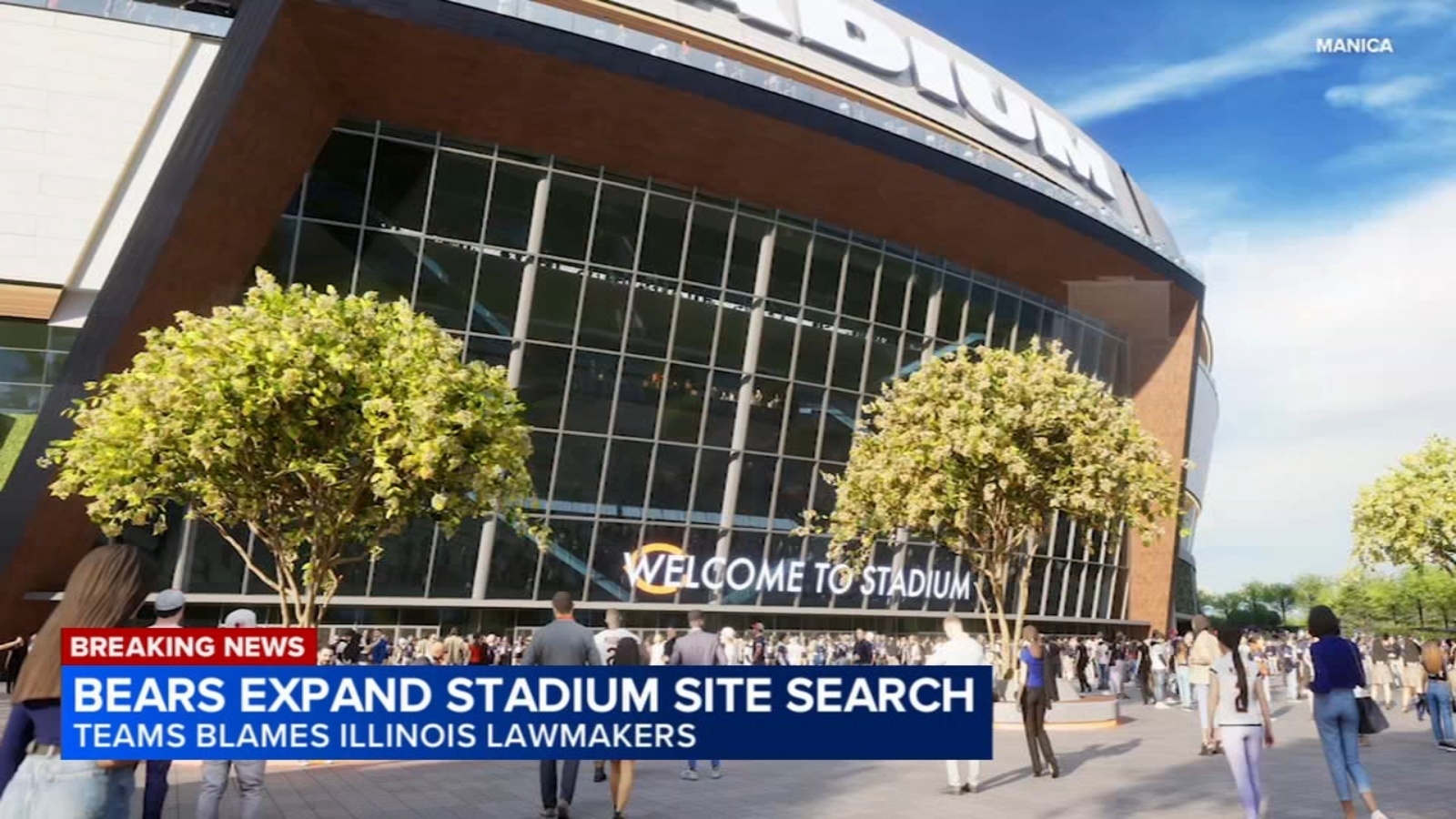

The Chicago Bears are broadening their search for a new stadium location beyond Arlington Heights, now considering options across the greater Chicagoland area and even into Northwest Indiana. This development was announced in an open letter from Bears President and CEO Kevin Warren on Wednesday.

Warren expressed frustration over the lack of collaboration with Illinois lawmakers concerning the infrastructure needed for their Arlington Heights stadium plans.

ABC7 Chicago is now streaming 24/7. Click here to watch

In his letter, Warren clarified that while the proposed stadium in Arlington Heights wouldn’t require Illinois taxpayer funding for its construction, the team is still seeking state assistance for developing the surrounding infrastructure.

“We’ve been informed by state leaders that our project won’t be a priority in 2026, despite the benefits it could bring to Illinois,” Warren stated. “Therefore, we must expand our search beyond Arlington Park and carefully evaluate opportunities throughout the wider Chicagoland region, including Northwest Indiana. This decision isn’t about leverage. We’ve spent years trying to establish a new home in Cook County, investing significant time and resources in evaluating multiple sites before choosing Arlington Heights.”

RELATED | Bill to entice the Chicago Bears to Northwest Indiana advances to the governor’s desk

A spokesperson for Governor JB Pritzker responded with a statement: “The suggestion that the Bears might relocate to Indiana is a surprising affront to the dedicated fans who have supported the team throughout this successful season. The Governor, a Bears enthusiast himself, has always wished for the team to remain in Chicago. While he acknowledges that, as a private business, the Bears will make their own decisions, he has also emphasized that no private development should place the financial burden solely on taxpayers.”

Cook County Board of Commissioners President Toni Preckwinkle shared the following statement:

“We’re proud to have recently hosted a productive meeting between the State, City and County and the Bears. It was important for us to bring everyone to the table and have a conversation around making a serious commitment to keeping the Bears in Cook County and Illinois. We’re shocked and disappointed that the Bears would discuss moving to Indiana at this time.”

The Bears said in a letter to lawmakers in October that they would set aside $25 million for Chicago and the Chicago Park District amid their stadium move to Arlington Heights.

The funds could be used for maintenance of Soldier Field, support of park district programs, paying any shortfall of Illinois Sports Facilities Authority bond payments or anything else, the letter said.

In October, State Rep. Kam Buckner called the offer not just “inadequate” but “disrespectful.”

“It reflects a longer pattern of tone-deafness from this franchise when it comes to its relationship with the city that made it,” he said. “We’re talking about a franchise valued at nearly $10 billion offering scraps to Chicago.”