Share this @internewscast.com

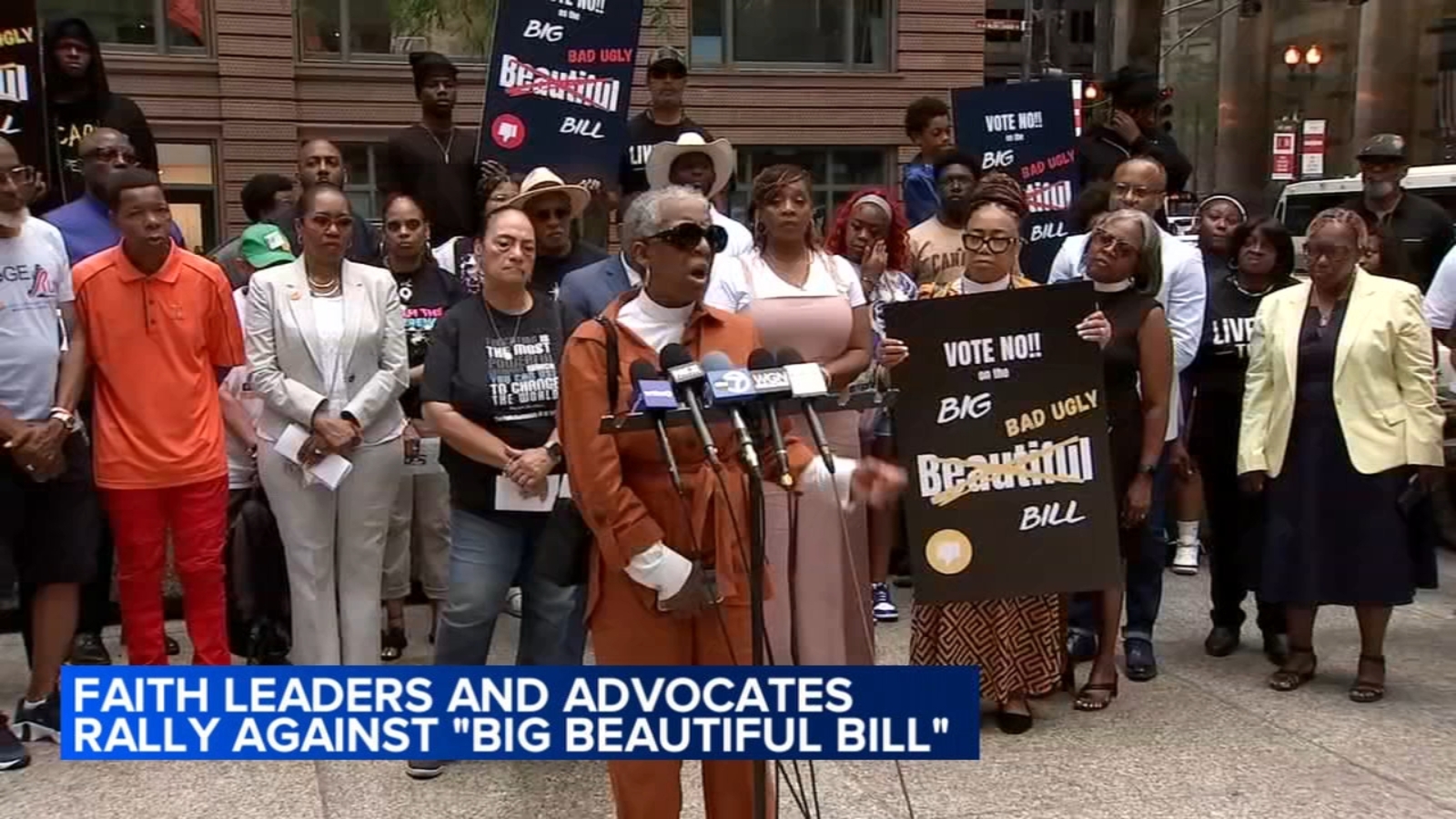

CHICAGO (WLS) — Protesters in Chicago gathered on Wednesday to express their disapproval of President Donald Trump’s extensive tax and spending plan, urging Congress to reject the proposal.

Trump’s bill is now in the hands of the House of Representatives with a good deal of uncertainty about its future.

ABC7 Chicago is now streaming 24/7. Click here to watch

There is a lot of political pressure being exerted on both sides of the debate on the bill.

President Trump and his supporters are striving to unify Republicans in favor of the bill, as Democrats and their allies put up a strong opposition to thwart its progress.

Religious leaders and politicians came together at Federal Plaza on Wednesday morning, united in delivering a firm message to Congress concerning the president’s touted major legislative initiative.

“This bill is not beautiful and is not particularly complicated. It is reverse Robin Hood. It is taking from the poor and giving to the rich,” the Rev. Marshall Hatch said.

Demonstrators renamed the mega-bill the “bad ugly bill.”

“Let me be clear: We do not care what party you belong to. If you support this bill, you will see us in your offices, at your town halls and your streets,” said Artinese Myrick, with Live Free.

There are concerns about how the bill would cut nutritional food assistance for the needy.

“We run a food pantry on 79th Street right now. By the end of each week, we run out of food. When the SNAP cuts and the Medicaid cuts go through, we will turn away probably approximately three to 400 people a week that we can no longer feed,” said Fr. Mike Pfleger, with St. Sabina Church.

There are also concerns about cuts to Medicaid and the fallout for safety net hospitals. The Congressional Budget Office estimates the bill will cost 11.8 million Americans their health care coverage over the next decade.

“If you’re a young mother raising young children and you’re on Medicaid, your Medicaid benefits are not going to change or be altered. If you’re a senior citizen and this is the only thing you rely on, is Medicaid, that’s not going to be altered or changed,” said Republican Rep. Darin LaHood, who represents central and northwestern Illinois.

LaHood says Medicaid will be cut for non-citizens and for able-bodied adults who can work.

Republicans also tout the fact the bill will eliminate taxes on tips and overtime.

“This may not be perfect for everybody. But, overall, it’s going to do a lot to get the economy back on track, to put more money in the pockets of working people,” LaHood said.

Democrats on Capitol Hill are vowing to fight.

“We are fighting for everyone in this bill, in this place. But let’s go, and let’s go vote hell no on the betrayal bill of Donald Trump,” said Democratic Rep. Delia Ramirez, who represents Chicago and the west suburbs.

What’s not clear is when there will be a vote on the bill.

Speaker Mike Johnson does not want to make any changes because then it would have to go back to the Senate for another vote.

So, for now, the standoff on Capitol Hill continues.

Copyright © 2025 WLS-TV. All Rights Reserved.