Share this @internewscast.com

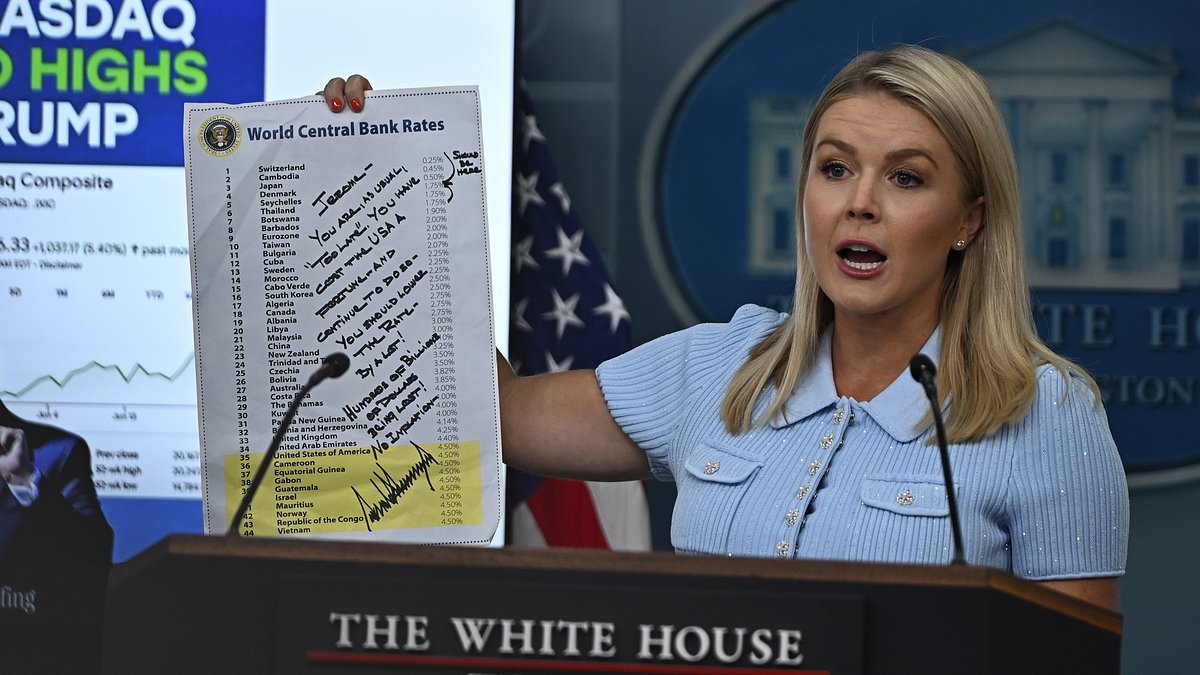

President Donald Trump is finding novel ways to try to pressure Fed chair Jerome Powell to lower interest rates – this time releasing an angry hand-written note online that casts the US central bank as behind the curve. Trump posted a chart of ‘World Central Bank Rates’ – showing institutions from countries including Botswana, Bulgaria, Cabo Verde, and Albania who have set their own rates lower than the U.S.

He hand-wrote the note in all-caps with his familiar Sharpie, once again telling Powell that he is ‘too late’ in bringing down rates. ‘You have cost the USA a fortune and continued to do so,’ he lectured, ‘and continue to lower the rate – by a lot!’ ‘Hundreds of billions of dollars being lost! No inflation ,’ the president added.’

Trump last week said he was already thinking of replacements for the Princeton-educated Powell, who he has repeatedly called ‘stupid.’ Trump published the post shortly before the White House press briefing, where press secretary Karoline Leavitt read from what she called ‘original correspondence’ from Trump.

‘As the President has consistently stated, the American economy is booming, and there were so many economic analysts who said that this President’s policies would drive our economy down, when in fact, we have seen the opposite,’ she said at the top of the briefing. ‘We’ve seen a massive deregulation campaign take place. We’ve seen inflation completely diminish from where it was under the reckless spending and the bad policies of the previous, incompetent administration.

‘The American people want to borrow money cheaply, and they should be able to do that, but unfortunately, we have interest rates that are still too high,’ Leavitt said. The president made clear where he thinks US rates should be. ‘Should be here,’ he wrote on his note, pointing to six countries with lower rates at the top of his list.

Powell himself testified last week that one reason the fed was reluctant to slash rates further were the Trump tariffs injecting uncertainty into the markets. He told the Senate Finance Committee: ‘We do expect to show up — tariff inflation to show up more.’

‘But I want to be honest, we really don’t know how much of that’s going to be passed through to the consumers. We just don’t know. And we won’t know until we see it. It could be lower than we expect; it could be higher. We have to wait and see, which is kind of what we’re doing.’ ‘Increases in tariffs this year are likely to push up prices and weigh on economic activity,’ Powell told members of the House Financial Services Committee in separate testimony.

In just one example, Trump last week said the US was ending trade talks with Canada after it imposed a digital services tax that could hammer US tech companies. Then Canada PM Mark Carney announced it was dropping the tax after Trump’s threat. Leavitt said the two men spoke Sunday night. She said Carney and Canada ‘caved to the United States of America.’

‘The President made his position quite clear to the prime minister, and the prime minister called the president last night to let the president to let the President know that he dropped that tax, which is a big victory for our tech companies and our American workers hear at home.’

‘At the top is Switzerland. They’re only paying a quarter for interest rates. Cambodia, Japan, Denmark, Thailand, Botswana, Barbados, Taiwan, Bulgaria, Cuba, Sweden, Morocco, Cabo Verde, South Korea, Algeria, Canada, Albania, Libya, Malaysia, China, New Zealand, Trinidad and Tobago, Czechia, Bolivia, Australia, Costa Rica, the Bahamas, Kuwait, Papua, New Guinea, Bosnia, United Kingdom and the UAE are all paying lower interest rates than the United States of America, which has one of the hottest and strongest economies in the world,’ she said.

Leavitt also read Trump’s letter aloud, concluding: ‘The President is right. There is historically low inflation thanks to his policies. And we will continue to drive down the cost of living in this country for Americans.’ Leavitt wouldn’t respond directly when asked why Trump wouldn’t just fire Powell, the chair of the independent Fed’s board of governors. But she did claim there had been ‘politicization of the Fed.’

‘Jerome Powell cut rates numerous times ahead of the election when Joe Biden was in his Oval Office, but now he refuses to when the economy is in a much better place.’ The Fed sometimes lowers its federal funds rate in order to try to boost economic activity, raising it to try to control inflation.