The Education Department announced Thursday that it will temporarily lower interest rates for certain federal student loan borrowers, an effort intended to make repayment more manageable as delinquencies reach their highest point in six years.

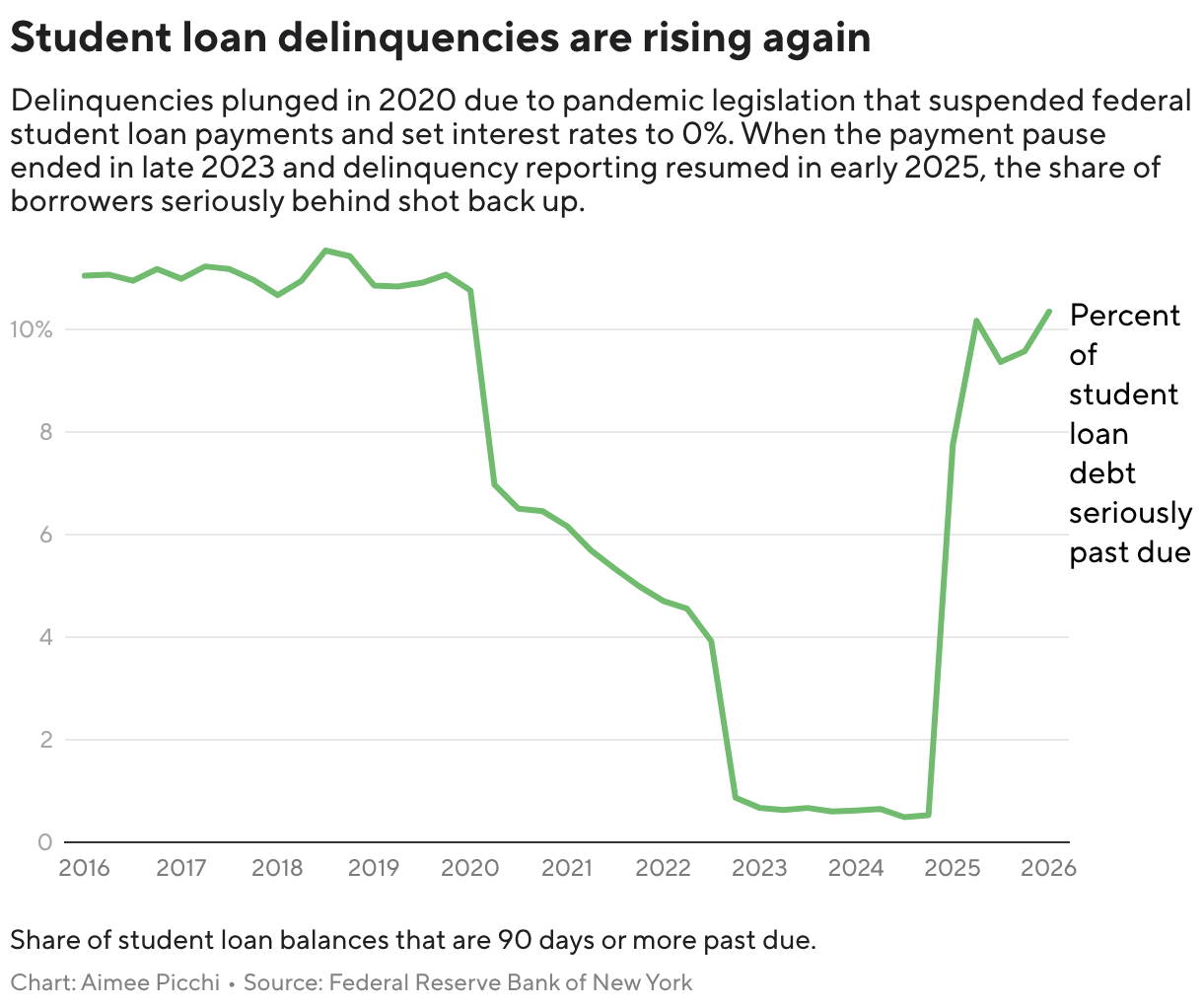

The move trims borrowing costs by 1 percentage point for a limited time. It comes as 10.3% of student loans were delinquent in the first quarter — the largest share in six years and roughly 20 times higher than the rate seen in mid-2024, according to the Federal Reserve Bank of New York.

Education Undersecretary Nicholas Kent described the adjustment as a step toward “making student loan repayment easier than ever” while also strengthening “the overall health of the federal student loan portfolio.”

That portfolio has grown to nearly $1.7 trillion, leaving millions of borrowers under pressure as they try to stay current on their payments.

The relief, however, will not be available to everyone, and borrowers seeking the lower rate must satisfy specific requirements. The announcement also comes as the Trump administration prepares to reshape student lending beginning July 1, including new caps on borrowing and changes to repayment choices.

Here is what to know about the interest-rate reduction and the broader policy backdrop:

Who is eligible for the interest rate reduction?

The temporary reduction applies only to a specific group: borrowers with federal Direct Loans issued after July 1, 2012, who are either already using automatic payments or enroll in auto pay.

For many borrowers, the change will not produce an immediate savings. Eligibility requires several steps, including enrolling in automatic payments and, for some borrowers, consolidating existing loans.

ALSO READ: What Happened To Alice Cottonsox: Is She Alive Or Dead? Wikipedia Bio Explored

Currently, just 40% of borrowers are enrolled in auto pay — a figure the department is hoping to increase with the new incentive of the interest rate reduction.

Nearly 9 million student loan borrowers are in default, meaning they’ve missed nine months of payments. For them to become eligible for the rate reduction, they must get back in good standing, typically by consolidating their loans and then applying for a new repayment plan.

What if you already have autopay set up?

For borrowers already enrolled in auto pay, the savings will be smaller.

Borrowers who currently use auto pay already receive an interest-rate discount of 0.25%, so the new reduction takes off just 0.75%.

When does the interest rate reduction end?

For all borrowers, the rate reduction will be temporary, lasting through June 30, 2028.