Share this @internewscast.com

During the holiday season, I stumbled upon a heated online discussion regarding the proposal to set the U.S. poverty line at $140,000. With only about 12 percent of individuals earning above this figure, adopting such a benchmark would imply that 88 percent of American workers live in poverty.

Numerous experts have already dissected the technical flaws of this proposal, leaving little for me to contribute in that regard. The notion is so absurd that it hardly warrants serious debate.

Yet, this scenario offers a revealing glimpse into the dynamics of populism. While many individuals have prospered over the years, populists argue that the majority are struggling. This rhetoric gains traction as Americans perceive that everyone else is facing hardship. Populist leaders exploit these fears, advocating for radical policy changes that often align with pre-existing biases.

However, the perception of universal hardship is misguided, and some populist policies threaten to undermine the prosperity that free enterprise economies typically enjoy. Such economies, characterized by openness to trade and immigration, outperform their insular, nationalistic counterparts. Despite clear data supporting this, populist politicians frequently scapegoat foreigners, corporations, and financial institutions for perceived widespread societal woes.

This brand of irrationality is not exclusive to the populism that emerged during the Trump era, nor is it confined to economic policy. Historical federal policies regulating financial markets illustrate how rapidly misguided ideas can spread, the risks they pose, and their enduring impact.

Free enterprise economies, with more openness to trade and legal immigration, do better than the closed off nationalistic alternatives. While the data on this point are clear, populist politicians have a long history of blaming foreigners, big business, and big finance for all the problems that are supposedly ruining everyone else’s lives.

Trump Populism Is Nothing New

None of this craziness is unique to Trump-era populism. Indeed, it’s not even unique to populist policy governing the overall economy. Federal policy regulating financial markets provides great historical examples of how quickly foolish ideas spread, how dangerous they can be, and how long they can last.

Perhaps the most salient example is the story surrounding the 2008 financial crisis, which was used to justify the Dodd-Frank Act. It’s still widely believed that the crisis was caused by deregulating financial markets during the 1980s and 1990s. But financial markets were not deregulated during any part of the 20th century, and the Dodd-Frank Act was largely a step in the wrong direction—it added tons of regulation but did little to address what caused the crisis.

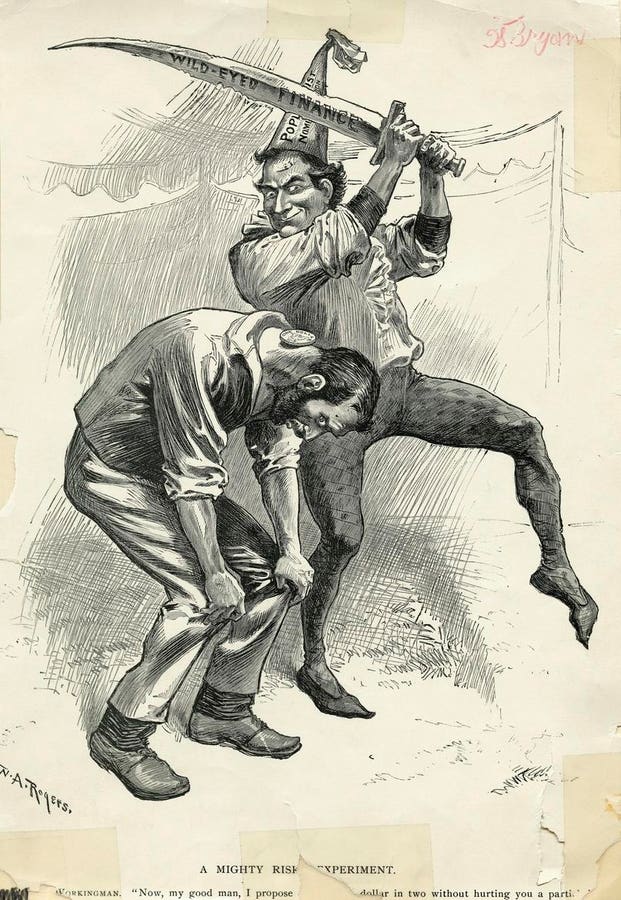

Aside from major crashes, centuries of history document the love-hate relationship people have with financial markets. That complex relationship, of course, makes it a rich target for populist agitation.

Populism Always Targets Financial Markets

Financial markets help level the economic playing field for people who are less well off—but only after they take on economic risk. Many of those risks don’t work out so well, so it’s not too surprising that people tend to distrust, if not hate, financial markets. But they shouldn’t hate financial markets because that risk is no different than the risk any business owner assumes when he or she invests in their business.

Even where learned people are supposed to objectively evaluate evidence, the status of the love-hate relationship doesn’t improve much.

For decades academics have smeared finance as unproductive and wasteful, if not outright dangerous and nefarious.

Even John Maynard Keynes, one of the best-known economists of all time, tarnished financial markets as the cause of the Great Depression on little more than a reflexive distaste. Decades later, Nobel prize winning economist James Tobin doubled down, complaining about derivatives and griping about the “speculations on the speculations of other speculators” in financial markets. But he, like Keynes, never defined how much was too much, or how to objectively separate out investments in “real” assets from speculation.

In 1998, Economics Nobel Laureate Merton Miller fought back. He argued that whether financial markets contribute to economic growth “is a proposition almost too obvious for serious discussion.” The evidence is very clear—countries with developed financial markets do better than those without them, and financial markets are inseparable from American prosperity. (It’s also kind of funny that, historically, American populist politicians complain about the financial industry and about the common man’s lack of access to credit.)

Still, people have believed in the story of rogue financial markets for decades. While this narrative runs against the grain of fact, it does explain why they believe most people aren’t very well off. Most often, they ignore the evidence in favor of things that just seem or sound right.

Populism Depends On Fiction

Trump-era populism is the culmination of those feelings, and it is rife with examples. In his 2020 book, “The Stakes: America at the Point of No Return,” author Michael Anton laments that his parents’ and grandparents’ California, the “greatest middle-class paradise in the history of mankind,” is long gone.

To support his assertion, Anton asks his readers to evaluate their lives through the lens of “The Brady Bunch,” the popular TV sitcom that ran from 1969 to 1974. It’s a clever idea because people, especially those over 40 years old, can easily identify with the show. It helps them connect with Anton’s idealized past, when “any man could earn a living and raise a family on one income almost anywhere.”

It should be obvious, but “The Brady Bunch” was a fabrication. It wasn’t about a real family or career. Unlike the show, it was very difficult—as it is now—to earn enough money to raise six children and have a live-in maid in a huge house in a southern California suburb.

Mike Brady was not a real architect, and the show does not tell us anything about how difficult life is now compared to 1970, for architects or anyone else. (And I do recall an episode where Carol complained about the high price of butter, but I digress.)

Fiction Makes Bad Policy

Anton’s book is just one example, and the latest blow up over the $140,000 poverty threshold idea shows just how unhinged this narrative of doom and despair has become.

The dangerous part, though, is that members of Congress and the White House are using these stories to implement dangerous policies. They’re not just having debates.

The core of the populist project is to essentially tear down the free-enterprise system and replace it with something entirely different. The administration wants direct government stakes in private companies, and they want to run a government patronage system for international trade, and to some extent immigration.

The whole thing is antithetical to the American experiment, and it will give government officials more control over Americans’ lives. That approach tends to work out poorly for the people who are not in power.

It’s even worse that these awful policies are based on fiction. Just like the Brady Bunch, they’re based on stories, and not particularly good ones. It’s hard to watch, even fifty years later.