Share this @internewscast.com

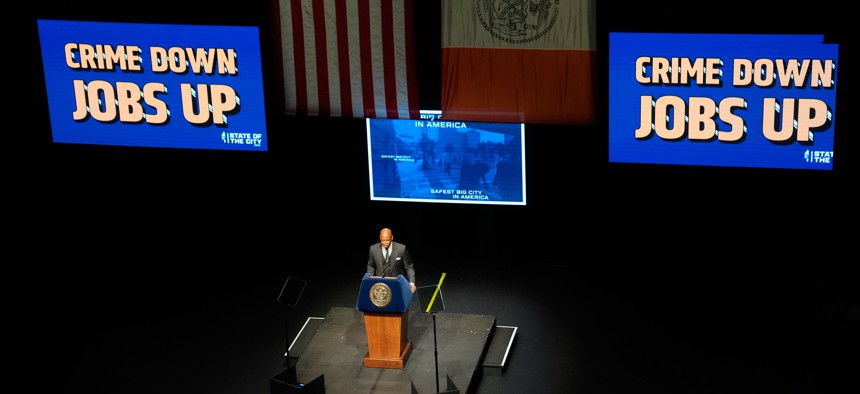

Mayor Eric Adams gave his third State of the City address at Hostos Community College in the Bronx, outlining his vision for the city. He stressed his administration’s focus on crime, economic opportunity, and the immigration situation in his speech. Adams said his administration aimed to increase public safety, the economy, and working-class livability.

Photo from Google

Promises Safety, Jobs, and Affordable Housing in 2024 Amid Progress and Crime Reduction

Adams noted progress in 2023 but stressed the need for more excellent work in his presentation. He promised to keep New Yorkers safe, create good-paying jobs, provide affordable housing, and support workers in 2024.

Adams pledged to revitalize the $400 million North Shore of Staten Island and referenced a Department of Education reading campaign. He told about a local woman who received city support in locating shelter after Hurricane Ida destroyed her home in 2021.

Citywide, the mayor stressed his administration’s focus on crime reduction since entering office. He cited a 12% drop in homicides and a 25% drop in gunshots as proof of their efforts. Adams believes safer streets will enhance economic prospects, supporting the administration’s target of 5 million employment by 2026.

READ ALSO: Massive Manhunt Ends In Tragic End: Suspect In 8 Murders Dies From Self-Inflicted Gunshot Wounds

Mayor Adams Advocates for Migrant Employment Amidst Citywide Vision for Safety and Prosperity

Adams urged the federal government to let the city’s tens of thousands of migrants work. He said that the federal government must intervene in a national crisis, even though the city has done its share.

Mayor Adams outlined his citywide plan, focusing on public safety, economic growth, and the immigration dilemma. The address shows the continuous commitment to enhancing New York City residents’ well-being and prospects.

READ ALSO: Suspect Apprehended: Evan Hughes, 60, Arrested In Homestead Shooting Case